Existing economic challenges will be further compounded by a predicted ‘second wave’ of negative economic impacts resulting from the coronavirus pandemic. But African governments, along with major global bodies, can play a decisive role through targeted policy interventions towards a sustainable post-pandemic recovery.

The severity of the pandemic and its long-term effects will largely be shaped by a key factor in Africa’s vulnerability – limited fiscal space. It is estimated that Africa could lose up to 20–30% of its fiscal revenue1AU, Impact of the Coronavirus (COVID-19) on the African Economy, report (Addis Ababa: AU Commission, 2020), https://www.tralac.org/news/article/14483-impact-of-the-coronavirus-covid-19-on-the-african-economy.html, which could result in an inability to service debt or even trigger a default. In November 2020, Zambia was the first African country to default on its loans.2Peter Fabricius, Zambia defaults, economically and politically. https://issafrica.org/iss-today/zambia-defaults-economically-and-politically

While wealthier economies have the luxury of historically low borrowing costs, most developing nations will find it extremely difficult and expensive to create the fiscal space necessary to fund health system expenditure, revenue losses and economic stimulus packages. This fiscal shortcoming presents a difficult moral trade-off between lives, livelihoods and debt – something that most African states are grappling with as the virus continues to spread.

The second wave

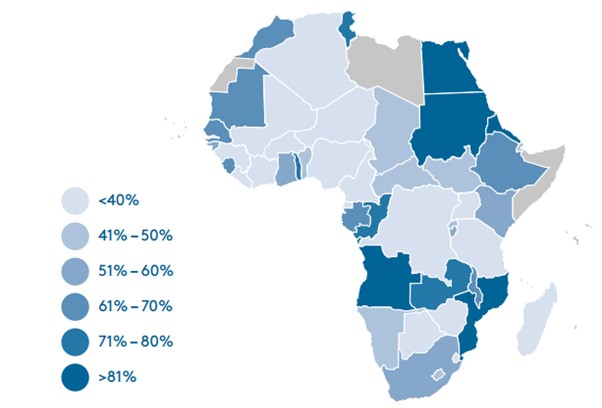

Left with no other options, African governments will turn to international markets, which may increase countries’ debt levels. A third of African countries are already, or are about to be, at high risk of being debt-distressed (>60% debt to GDP), owing to recent sharp increases in their debt levels (Figure 1). Debt should be used for productive investment.

However, given current circumstances, African countries need external sources of finance to support their weak healthcare systems and to prevent socioeconomic fallout.

Major global credit ratings agencies will have a decisive influence on COVID-19’s impact on African countries. Many states have already witnessed their ratings being lowered and further downgrades could average declines of three investment grades for weaker economies and one investment grade for countries with strong fundamentals.3CountryRisk.io, The Second Wave: The Impact of Covid-19.

From a debt sustainability perspective, the downgrades are the result of an immediate economic contraction, the initial debt-to-GDP ratio, the accumulation of new debt (which widens current fiscal deficits) and the real interest repayment on debt.

If economies follow a V-shaped recovery path, the number of actual downgrades could be small. However, in the event of a protracted economic decline, more downgrades could still materialise.4CountryRisk.io, The Second Wave: The Impact of Covid-19.

Since March 2020, COVID-19 has already triggered rating downgrades in seven of the 19 rated sub-Saharan African countries, including in some of Africa’s biggest economies.5African Market News, ‘Fitch Ratings, Fitch: Outlook on sub-Saharan Sovereigns Is Negative’ (13 June 2020), https://www.fitchratings.com/research/sovereigns/outlook-on-sub-saharan-sovereigns-is-negative-12-06-2020 S&P and Moody’s downgraded Ghana’s economic outlook to negative, with the latter affirming the country’s long-term local and foreign-currency issuer and foreign-currency senior unsecured bond ratings at B3. Ghana is vulnerable to shocks because of its high reliance on external financing, both in local and foreign currency, and very weak debt affordability.

Moody’s and Fitch downgraded Angola to B- with a stable outlook, reflecting the impact of lower oil production and lower oil prices, together with a sharp depreciation of the Kwanza (which has increased debt levels and debt servicing costs, while reducing international reserves).

S&P revised Nigeria’s outlook to negative, citing the size of the country’s debt and falling reserves, among other factors. Fitch downgraded Nigeria’s long-term foreign-currency issuer default rating (IDR) to B (with a negative outlook) and Zambia’s IDR to CCC.6Ridle Markus (Africa Strategist at Absa Corporate and Investment Banking), interviewed by Consumer News and Business Channel (CNBC) News Africa (9 March 2020).

These downgrades are attributed to rising risks associated with COVID-19 and these governments’ inability to find funding to cushion their economies while continuing to service their current debts.

Figure 1 – General government gross debt (2018, % of GDP)

One avenue for recourse for African economies would be for credit ratings agencies to suspend their assessments for developing countries until global production and supply chains return to pre-COVID-19 levels.

Other global roleplayers, such as the UN’s $2 billion fund to help the world’s poorest countries fight the pandemic, or the G20’s Debt Service Suspension Initiative will also aid African countries in bridging their current financing gap.

Containing the impact – government policy options

African governments also have a decisive role to play in the post-pandemic recovery. The introduction of aggressive stimulus packages by advanced and emerging economies’ central banks7https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19far exceeding conventional interest rate cuts – has resulted in synchronised actions that have helped generate the monetary space needed by developing economies. This increased space will enable them to use monetary policy instruments and macroprudential policy to respond to domestic cyclical conditions.

African central banks also have a vital role to play in managing the economic fallout from the pandemic. Central banks are the only institutions in developing countries that have balance sheets strong enough to prevent the collapse of the private sector, using monetised deficit-financed interventions. In instances where they are financed through standard government debt, interest rates would have to rise sharply.8Nouriel Roubini, ‘This Is What the Economic Fallout from Coronavirus Could Look Like,’ WEF (6 April 2020), https://www.weforum.org/agenda/2020/04/depression-global-economy-coronavirus/

“African policymakers, together with key global financial actors and partners, are not without options to steer their economies towards a sustainable recovery”

Furthermore, in the interests of promoting financial stability, macroprudential authorities would do well to encourage banks to allow distressed borrowers to renegotiate their loan terms, while absorbing the costs of such restructuring by drawing on their capital buffers. Banks must continue to lend to illiquid but still-solvent small and medium enterprises.

In parallel, authorities should tightly monitor the banking sector’s asset quality to determine the amount of fiscal support – for example, equity injections – that will be required should the effects of the downturn persist.

The COVID-19 pandemic has been a major economic disruptor across the globe and more so in African countries where it has exposed structural economic deficiencies. Yet, African policymakers, together with key global financial actors and partners, are not without options to steer their economies towards a sustainable recovery.

This article draws on a research brief undertaken as part of the COVID-19 Macroeconomic Policy Research in Africa (CoMPRA) project. See www.CoMPRAfrica.org for related research.